Circular No. 109/2018/TT-BTC guiding the accounting regime applicable to the Debt Repayment Accumulation Fund, effective from January 1, 2019. The Circular stipulates accounting vouchers, accounting accounts, accounting books, and financial reports, applicable to the Department of Debt Management and Foreign Financial Affairs - Ministry of Finance and related organizations and individuals.

Đối tượng áp dụng

The Department of Debt Management and Foreign Financial Affairs - Ministry of Finance and related organizations and individuals.

Các điểm cốt lõi

- The Debt Repayment Accumulation Fund must establish accounting vouchers for all economic and financial transactions; use the Vietnamese Dong as the monetary unit; apply annual and quarterly accounting periods; maintain general and detailed accounting books.

- The Department of Debt Management and Foreign Financial Affairs is responsible for managing and using accounting information and documents; organizing the accounting staff; preparing periodic quarterly and annual financial reports.

- The Debt Repayment Accumulation Fund must apply the system of accounting vouchers, accounts, books, and financial reports as prescribed in this Circular.

- Accounting vouchers must bear signatures of the signatories; be prepared by computer or handwritten; shall not be erased or abbreviated.

- Accounting books must be recorded continuously from the time they are opened until they are closed, ensuring timeliness, clarity, and completeness.

🌐 Tác động xã hội từ văn bản này

- Positive impact: Strengthening financial management and transparency in the operations of the Debt Repayment Accumulation Fund.

- Negative impact: It may impose a cost burden on organizations and individuals required to comply with the regulations.

❓ Câu hỏi thường gặp

When does the Debt Repayment Accumulation Fund establish accounting vouchers?

All economic and financial transactions related to the activities of the Fund must establish accounting vouchers.

What is the monetary unit used in the accounting of the Debt Repayment Accumulation Fund?

The monetary unit is the Vietnamese Dong (national symbol is 'đ', international symbol is 'VND').

The annual accounting period of the Debt Repayment Accumulation Fund includes which months?

The annual accounting period consists of twelve months, from the first day of January to the last day of December of the Gregorian calendar year.

What responsibilities does the Department of Debt Management and Foreign Financial Affairs have in preparing financial reports?

The Department of Debt Management and Foreign Financial Affairs must prepare and submit periodic quarterly and annual financial reports.

What is the deadline for submitting financial reports of the Debt Repayment Accumulation Fund?

Quarterly financial reports must be submitted no later than the tenth day of the first month of the quarter following the reporting quarter; Annual financial reports must be submitted no later than March 31 of the year following the reporting year.

Toàn văn

|

MINISTRY OF FINANCE ---------------------------- Number: 109/2018/TT-BTC |

SOCIALIST REPUBLIC OF VIET NAM Hanoi, November 15, 2018 |

CIRCULAR

Guidelines on accounting regulations applicable to the Debt Repayment Reserve FundCommission for Debt Repayment Accumulation

Pursuant to the Law on Public Debt Management dated November 23, 2017;

Pursuant to the Accounting Law dated November 20, 2015;

Pursuant to the Law on State Budget dated June 25, 2015;

Pursuant to Decree No. 94/2018/NĐ-CP dated June 30, 2018 of the Government on public debt management operations;

Pursuant to Decree No. 97/2018/NĐ-CP dated June 30, 2018 of the Government on lending out foreign official development assistance (ODA) loans and concessional foreign loans;

Pursuant to Decree No. 92/2018/NĐ-CP dated June 26, 2018 of the Government on management and use of the Debt Repayment Reserve Fund;

Pursuant to Decree No. 174/2016/NĐ-CP dated December 30, 2016 of the Government detailing certain provisions of the Accounting Law;

Based on Decree No. 71/2007/NĐ-CP dated May 3, 2007 of the Government detailing certain provisions of the Law on Information Technology concerning the information technology industry;

Pursuant to Decree No. 87/2017/NĐ-CP dated July 26, 2017, issued by the Government, stipulating the functions, tasks, powers, and organizational structure of the Ministry of Finance;

At the proposal of the Director of the Department of Management and Supervision of Accounting and Auditing,

The Minister of Finance issues this Circular guiding the accounting regulations applicable to the Debt Repayment Reserve Fund.

PART I

GENERAL PROVISIONS

Article 1. Scope of Regulation

This Circular stipulates accounting vouchers, accounting accounts, accounting ledgers, financial statements, and other organizational aspects of accounting work for recording economic and financial transactions related to the activities of the Debt Repayment Reserve Fund as prescribed by law.

Article 2. Applicability

This Circular applies to the Department of Debt Management and External Finance - Ministry of Finance and relevant organizations and individuals.

Article 3. Tasks of the Debt Repayment Reserve Fund's accountant

The accountant of the Debt Repayment Reserve Fund shall have the following tasks:

1. Collecting, processing, checking, monitoring, and analyzing information on the recovery of domestic re-lending debts from foreign loans of the Government; collecting risk reserves for re-lending; collecting re-lending management fees; government guarantee fees and late payment penalties for such guarantees (if any) to ensure repayment of foreign loans for re-lending by the Government; recovering capital advances from the Debt Repayment Reserve Fund; revenues from debt restructuring and portfolio management operations; interest income from deposits, loans, entrusted fund management, and investments by the Fund, and other revenues as prescribed.

2. Collecting, processing, checking, monitoring, and analyzing information on the repayment of foreign debts (including principal, interest, and fees (if any)) for re-lending loans; the use of capital advances to repay foreign debts for re-lending loans and government guarantees according to the Prime Minister’s decision; expenses for public debt management operations; loans to the State budget, idle funds investment, purchase of government bonds as prescribed by the Public Debt Management Law and Decree No. 92/2018/NĐ-CP, and other expenses as prescribed.

3. Monitoring risk reserves, handling potential risks that may occur when the Government guarantees enterprises and credit institutions' foreign loans, and expenditures for managing the Fund.

Article 4. Accounting methods for the Debt Repayment Reserve Fund

The accounting for the Fund must be carried out in accordance with the methods and principles prescribed in the Accounting Law, Decree No. 174/2016/NĐ-CP dated December 30, 2016 of the Government detailing certain provisions of the Accounting Law (hereinafter referred to as Decree No. 174/2016/NĐ-CP), and the guidance provided in this Circular.

Article 5. Units of measurement used in the accounting of the Debt Repayment Reserve Fund

1. The currency unit is the Vietnamese Dong (national symbol is "đ", international symbol is "VND"). In cases where foreign currencies arise, separate ledgers must be maintained in the original currency on Account 007 "Various Foreign Currencies" and converted to Vietnamese Dong at the prescribed exchange rate.

2. When preparing consolidated financial statements and consolidated management reports, if the reported figures exceed nine digits, thousand Vietnamese Dongs can be used as the shortened currency unit; if they exceed twelve digits, million Vietnamese Dongs can be used; if they exceed fifteen digits, billion Vietnamese Dongs can be used.

3. When using shortened currency units, rounding off should be done as follows: if the digit following the shortened currency unit is five or more, it should be increased by one; if it is less than five, it should not be counted.

Article 6. Accounting Periods of the Debt Repayment Accumulation Fund

The accounting periods include annual accounting periods and quarterly accounting periods, which are defined as follows:

1. An annual accounting period consists of twelve months, from the first day of January to the last day of December of the Gregorian calendar year.

2. A quarterly accounting period consists of three months, from the first day of the first month of the quarter to the last day of the last month of the quarter.

Article 7. Financial and Accounting Self-Inspection

1. The Fund shall be subject to inspection regarding the content of accounting work, accounting organizational structure, and accountants according to the decision of the Minister of Finance.

2. Annually, the Department of Debts and Foreign Financial Management must conduct financial and accounting self-inspection of the Fund in accordance with current laws on financial and accounting self-inspection.

Article 8. Responsibility for Managing Transaction Accounts and Activities of the Debt Repayment Accumulation Fund

The Fund shall open transaction accounts denominated in foreign currency and Vietnamese dong at the State Treasury or commercial banks in accordance with Clause 4, Article 2 of Decree No. 92/2018/ND-CP dated June 26, 2018 of the Government on the management and use of the Debt Repayment Accumulation Fund.

Article 9. Responsibilities for Managing, Using, and Providing Accounting Information and Documentation

1. The Department of Debts and Foreign Financial Management shall establish regulations on managing, using, and preserving accounting documentation, clearly defining responsibilities and authorities for each department and each accountant; it must ensure adequate physical facilities and means for managing and preserving accounting documentation.

2. The Department of Debts and Foreign Financial Management has the responsibility to provide timely, complete, and truthful accounting information and documentation to state agencies authorized to perform their functions under the law. Agencies receiving accounting documentation must have the responsibility to maintain and preserve the documentation during its use and must return all used accounting documentation fully and on time.

3. The provision of information and documentation to specific entities shall be decided by the Director of the Department of Debts and Foreign Financial Management in accordance with the law. The exploitation and use of accounting documentation must be approved in writing by the Director of the Department of Debts and Foreign Financial Management or the person authorized.

Article 10. Accounting Organizational Structure

The Department of Debts and Foreign Financial Management shall organize an accounting structure to implement the accounting system applicable to the Debt Repayment Accumulation Fund, appointing account managers and Chief Accountants (or persons responsible for accounting) in accordance with Decree No. 92/2018/ND-CP dated June 26, 2018 and Decree No. 174/2016/ND-CP dated December 30, 2016.

Chapter II

ACCOUNTING DOCUMENTS

Article 11. General Provisions on Accounting Documents

1. Accounting documents shall be implemented in accordance with the Accounting Law and Decree No. 174/2016/ND-CP.

2. Specific contents are stipulated in Articles 12, 13, and 14 of this Circular.

Article 12. Preparation of Accounting Documents

1. All economic and financial transactions related to the activities of the Fund must be recorded in accounting documents. An accounting document shall only be prepared once for each economic and financial transaction.

2. The content of the document must be clear and truthful to the content of the economic and financial transaction.

3. Writing on the document must be clear, without erasures or abbreviations.

4. The amount written in words must match the amount written in figures.

5. Accounting documents must be prepared with the required number of copies as specified for each document. For documents requiring multiple copies, they must be prepared in one go for all copies with the same content using a computer, typewriter, or carbon paper. In special cases where multiple copies cannot be prepared in one go, two separate preparations may be made but the content of all copies of the document must be identical.

6. Accounting documents prepared by computer must comply with the prescribed content and legal validity for accounting documents. Accounting documents used as direct bases for recording in accounting ledgers must contain accounting entries.

Article 13. Signing Accounting Documents

1. All accounting documents must have complete signatures according to the designated position on the document to be valid for implementation. Specifically, electronic accounting documents must have an electronic signature as prescribed by law. All signatures on accounting documents must be signed with a ballpoint pen or ink pen, not with red ink, pencil, or pre-carved signature stamps. Signatures on accounting documents used for payment must be signed individually per each copy. The signatures on accounting documents of one person must be consistent and must match the registered signature according to regulations; if no signature has been registered, subsequent signatures must be consistent with previous signatures.

2. The signature of the Director of the Debt Management and External Finance Department (or authorized representative), the Chief Accountant (or authorized representative), and the stamp on the document must correspond to the sample stamp and signature still in effect registered at the State Treasury or commercial bank. The signature of the accountant on the document must match the signature in the book of registered sample signatures. The Chief Accountant (or authorized representative) may not sign on behalf of the Director of the Debt Management and External Finance Department. An authorized representative may not re-authorize another person.

3. The Debt Management and External Finance Department must open a book to register the sample signatures of the cashier, accounting staff, Chief Accountant (and authorized representatives), Director of the Debt Management and External Finance Department (and authorized representatives). The book of registered sample signatures must be numbered and sealed with a cross-stamp by the Director of the Debt Management and External Finance Department (or authorized representative) for easy inspection when necessary. Each person must sign three sample signatures in the registration book.

4. When creating accounting documents on a computer, the numbering of the documents is automatically performed by the system. The accounting staff responsible for printing and presenting the documents to the head of the unit or authorized representative must sign according to their authority.

5. Accounting documents shall not be signed before recording or fully recording the content of the document according to the responsibility of the signer. The delegation of signing on accounting documents is regulated by the Director of the Debt Management and External Finance Department in accordance with the law, management requirements, ensuring strict control and asset safety.

Article 14. Procedure for Circulation and Inspection of Accounting Documents

1. Accounting documents created by the Fund or received from outside must be centralized in the accounting department of the Fund. The accounting department must inspect all such accounting documents and only after verifying their legal validity can they be used to record in the accounting books. The circulation procedure of accounting documents includes the following steps:

- Creating, receiving, and processing accounting documents;

- Inspectors and the Chief Accountant check and sign the accounting documents or present them to the Director of the Debt Management and External Finance Department for approval according to the regulations in each type of document (if applicable);

- Classify, arrange accounting documents, determine accounts, and record in the accounting books;

- Store and preserve accounting documents.

2. Content of inspection of accounting documents:

- Verify the clarity, truthfulness, and completeness of the indicators and elements recorded on the accounting documents;

- Verify the legality of the economic and financial transactions recorded on the accounting documents; compare the accounting documents with related documents;

- Verify the accuracy of the figures and information on the accounting documents.

3. When inspecting accounting documents, if violations of policies, systems, and regulations on economic and financial management by the State are discovered, they must be refused and reported immediately in writing to the Director of the Debt Management and External Finance Department for timely handling in accordance with current laws.

4. For accounting documents that are not properly prepared, with unclear content and figures, the person responsible for inspection or recording must return them, request additional procedures, and adjust them before using them as a basis for recording.

5. The list, model, explanation of content, and method of preparing accounting documents are specified in Appendix 01 "Accounting Document System" issued together with this Circular.

Chapter III

ACCOUNTS FOR ACCOUNTING

Article 15. Accounting Accounts and Accounting Account System

1. The accounting account system of the Fund includes accounts within the Balance Sheet and accounts outside the Balance Sheet, reflecting regularly and continuously the income and expenditure situation according to classification and systematically. Accounting accounts are opened for each accounting subject with distinct economic content.

2. Accounts within the Balance Sheet reflect all economic and financial transactions occurring according to accounting subjects including assets, sources of asset formation, and the movement process of assets at the Fund. The bookkeeping principle for accounts within the Balance Sheet is implemented using the "double-entry" method, where recording on the Debit side of one account must be simultaneously recorded on the Credit side of another account or multiple accounts, or vice versa.

3. Accounts outside the Balance Sheet reflect economic indicators already reflected in accounts within the Balance Sheet but require monitoring to serve management needs. The bookkeeping principle for accounts outside the Balance Sheet is implemented using the "single-entry" method, where recording on one side of an account does not require corresponding entries on the other side of other accounts.

Article 16. Classification and Application of the Accounting Account System

1. The accounting account system applicable to the Fund, as prescribed by the Ministry of Finance, consists of 16 accounts within the Balance Sheet and 01 account outside the Balance Sheet.

- Accounts within the Balance Sheet include: Level 1 accounts consisting of three decimal digits; Level 2 accounts consisting of four decimal digits (the first three digits represent Level 1 accounts, the fourth digit represents Level 2 accounts).

- Accounts outside the Balance Sheet consist of three digits, starting with the digit 0.

2. The Department of Debt Management and Foreign Financial Affairs must base its accounting records on the accounting account system issued in this Circular, and may supplement additional accounts in the following cases:

- Supplement detailed accounts for accounts already specified in the list of the accounting account system (Annex No. 02) accompanying this Circular to meet management requirements of the unit.

- In case of supplementing accounts at the same level as those already specified in the list of the accounting account system (Annex No. 02) accompanying this Circular, it must obtain written approval from the Ministry of Finance before implementation.

3. The list of accounting accounts, explanations of content, structure, and accounting methods is stipulated in Annex 02 "Accounting Account System" accompanying this Circular.

Chapter IV

ACCOUNTING LEDGER SYSTEM

Article 17. Accounting Ledger

1. The Fund opens general ledger and detailed ledgers to reflect all income and expenditure activities and management of the Fund. No income or expenditure of the Fund can be left unrecorded in the ledger.

2. Opening, closing, and correcting the accounting ledger shall be carried out in accordance with the provisions of the Accounting Law and Decree No. 174/2016/NĐ-CP dated December 30, 2016 of the Government detailing certain provisions of the Accounting Law.

3. Recording in the accounting ledger must ensure timeliness, clarity, and completeness according to the contents of the ledger. Information and figures recorded in the ledger must be accurate, truthful, and consistent with accounting vouchers.

4. Recording in the accounting ledger must follow the chronological sequence of economic and financial transactions. Information and figures recorded in the ledger of the subsequent year must continue the information and figures recorded in the ledger of the preceding year. The ledger must be recorded continuously from opening to closing.

5. The ledger must be strictly managed, with clear assignment of individual responsibilities for keeping and recording. Whoever is assigned the ledger must be responsible for everything recorded in the ledger during their period of custody and recording.

6. When there is a change in personnel responsible for keeping and recording the ledger, the Chief Accountant or the person in charge of accounting must organize the handover of management and recording responsibilities between the old and new accounting staff. The old accounting staff must be responsible for everything recorded in the ledger during their period of custody and recording. The new accounting staff will be responsible from the date of handover. The handover record must be signed and confirmed by the Chief Accountant or the person in charge of accounting.

Article 18. Accounting Method

1. The Debt Repayment Reserve Fund shall apply the Bookkeeping Voucher accounting method.

a) Principles for recording under the Bookkeeping Voucher accounting method:

- Record according to the chronological sequence of economic and financial transactions on the Bookkeeping Voucher Register;

- Record according to the economic content of the economic and financial transactions on the General Ledger.

b) Types of accounting books:

- Bookkeeping vouchers;

- Bookkeeping Voucher Register;

- Detailed accounting books.

2. The list of accounting books, book templates, and explanations of the accounting bookkeeping methods are stipulated in Appendix No. 03 "Accounting System" issued together with this Circular.

Chapter V

FINANCIAL REPORTING SYSTEM

Article 19. Responsibilities of the Department of Debt Management and Foreign Financial Affairs in preparing and submitting financial reports

1. The Department of Debt Management and Foreign Financial Affairs shall be responsible for preparing and submitting periodic quarterly and annual financial reports.

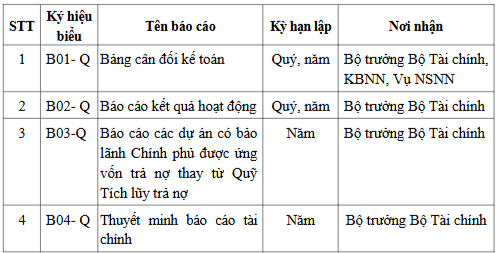

2. The list of financial reports applicable to the Debt Repayment Reserve Fund:

3. In addition to the financial reports prescribed in the above list, the Department of Debt Management and Foreign Financial Affairs must also prepare other reports as required by the management and operation of the Minister of Finance.

4. Templates for financial reports and explanations of the methods for preparing financial reports are stipulated in Appendix No. 04 "Financial Reporting System" issued together with this Circular.

Article 20. Requirements for Preparing and Presenting Financial Reports

1. The preparation of financial reports must ensure truthfulness, objectivity, completeness, timeliness, and accurately reflect the asset status, liabilities, revenues, and expenditures of the Fund.

2. The preparation of financial reports must be based on data after closing the accounting books. Financial reports must be prepared in accordance with their content, methods, and presented consistently across reporting periods.

3. Financial reports must be signed and stamped by the preparer, the Chief Accountant, and the Director of the Department of Debt Management and Foreign Financial Affairs before submission to the competent authority or publicized in accordance with the provisions of the law.

Article 21. Deadline for Submitting Financial Reports

1. Quarterly financial reports must be submitted no later than the 10th day of the first month of the following quarter.

2. Annual financial reports must be submitted no later than March 31 of the year following the reporting year.

Chapter VI

IMPLEMENTATION

Article 22. Effectiveness

1. This Circular takes effect from January 1, 2019.

2. This Circular replaces Circular No. 170/2014/TT-BTC dated November 14, 2014, guiding accounting for the Debt Repayment Reserve Fund.

Article 23. Implementation Organization

The Director of the Department of Accounting and Auditing Supervision, the Director of the Department of Debt Management and Foreign Financial Affairs, and the heads of related units are responsible for guiding and implementing this Circular./.

|

Place of Receipt: |

DEPUTY MINISTER |

Văn bản gốc (PDF)

Bản đồ quan hệ

Bấm vào một văn bản để mở. Viền đỏ = quan hệ làm thay đổi hiệu lực.

Bản dịch

Văn bản này có sẵn ở các ngôn ngữ sau: